Understanding your Debt-to-Income Ratio (DTIR) is one of the most important steps in managing your personal finances. Whether you're applying for a mortgage, a car loan, or simply trying to get a clearer picture of your financial health, your DTIR is a critical number that lenders use to evaluate your ability to manage monthly payments.

This guide walks through the Debt-to-Income Ratio Calculator—a simple yet powerful Excel tool designed to help you calculate your DTIR instantly, understand what the number means, and take action based on your results.

Your Debt-to-Income Ratio is the percentage of your gross monthly income that goes toward paying your monthly debts. Lenders use this ratio to assess your ability to manage new debt. A lower DTIR indicates a good balance between debt and income, while a higher DTIR suggests you may be overextended.

The formula is simple: Total Monthly Debt Payments divided by Total Monthly Income, multiplied by 100.

This file consists of a single worksheet that is clean, intuitive, and easy to use:

The template uses a simple color-coded system to show you exactly where you stand and what to do next.

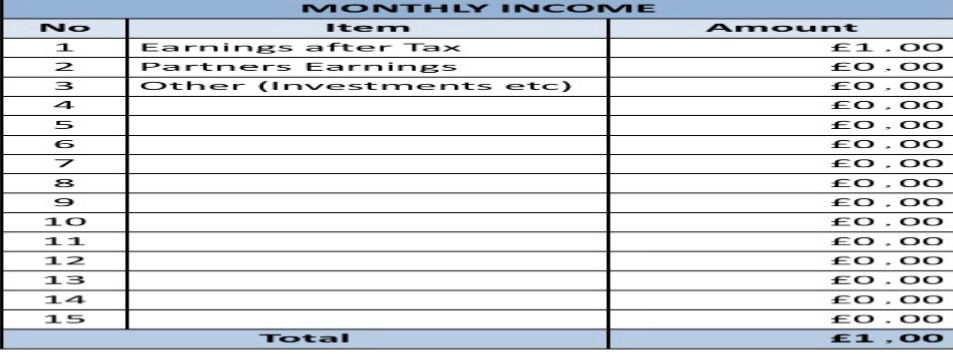

Caption: Enter all sources of monthly income in the blue fields, including your after-tax earnings, partner's earnings, and any investment or other income. The template totals them automatically.

Start by listing all sources of monthly income you receive. The template provides 15 lines, but you'll likely only need a few. Common income sources include:

Enter each amount in the column provided. The template automatically calculates your total monthly income at the bottom.

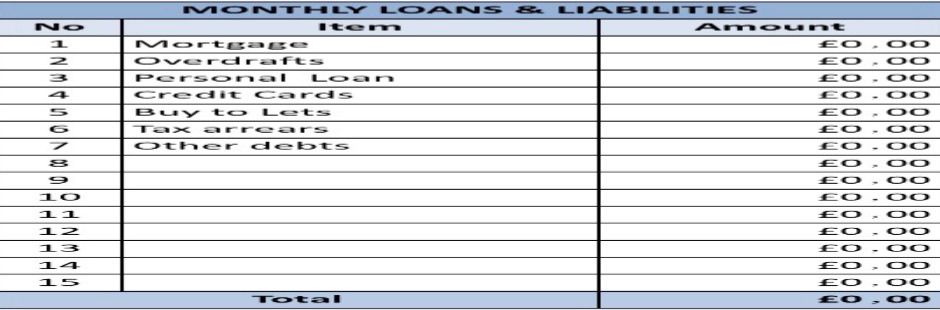

Caption: List all your monthly debt obligations, including mortgage payments, credit card minimums, personal loans, and any other recurring debts.

Next, list all your monthly debt obligations. The template includes common categories, but you can use the blank lines for any additional debts:

Be honest and thorough. Including all your debts gives you an accurate picture of your financial situation.

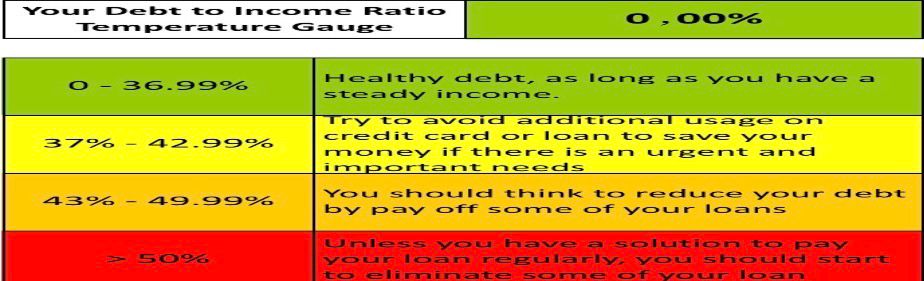

Caption: The temperature gauge automatically calculates your ratio and places you in one of four color-coded zones with specific guidance for each.

Once you've entered your income and debts, the template instantly calculates your Debt-to-Income Ratio and displays it prominently. More importantly, it places you in one of four zones with clear guidance:

The template doesn't just give you a number—it provides actionable guidance. Depending on your zone, you may need to:

Your DTIR is one of the most important numbers in your financial life for several reasons:

If your DTIR is higher than you'd like, here are practical steps to improve it:

What is a good Debt-to-Income Ratio?

Generally, a DTIR below 36 percent is considered good. Below 43 percent is acceptable for most mortgages. Above 50 percent is considered risky.

Should I use gross income or net income?

This template uses earnings after tax, which is your net income. This is more conservative and reflects what you actually have available to pay bills. Some lenders use gross income, so be consistent with whatever method you choose.

Do I include all debts or just major ones?

Include all monthly debt obligations. Credit card minimum payments, car loans, student loans, and even child support should be included. The more accurate your input, the more useful your result.

What if my income varies each month?

If your income fluctuates, use an average of the last three to six months. Be conservative in your estimate to ensure you're not overestimating your ability to handle debt.

How often should I calculate my DTIR?

Calculate your DTIR whenever your income changes significantly, when you take on new debt, or at least once per year as part of your financial checkup.

Your Debt-to-Income Ratio is a powerful measure of your financial health. This simple calculator takes the guesswork out of the equation, giving you an instant result with clear, actionable guidance based on your specific situation.

Whether you're preparing to apply for a mortgage, checking your financial fitness, or working toward a debt-free future, knowing your DTIR is the first step. Use this template regularly to track your progress and make informed financial decisions.

Download the template, gather your income and debt information, and see where you stand today. The number might surprise you—and more importantly, it might motivate you to take action.

Download your template:

Download Excel Template